Key Highlights

- The increasing influence of private equity, land banking, and international interest and investment have diversified the home builder consolidation landscape, fueling deal activity and valuation growth.

- Fewer homes are being built as top builders prioritize profitability over volume, potentially limiting housing options for consumers.

- Recent regulatory attention, including federal merger guidelines and oversight, assess whether market dominance by large builders impacts competition and affordability.

This article first appeared in the May/June 2026 issue of Pro Builder.

Anyone who pays even a little attention to the U.S. housing industry knows that consolidation among home builders has been going on for a generation or more … and shows no sign of slowing down.

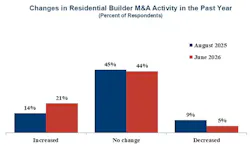

In fact, as we gathered responses for our annual Top 200 rankings of home builders by their 2025 revenue, merger and acquisition (M&A) activity among builders was at a fever pitch, led by Berkshire Hathaway (parent company of 13th-ranked Clayton Properties Group) making a reported $8.5 billion offer to buy #6 Taylor Morrison late last month.

Earlier this year, Sumitomo Forestry announced a $4.5 billion acquisition of #17 Tri Pointe Homes, while #21 Stanley Martin Homes—bought by Japan-based Daiwa House in 2017—was set to acquire #67 United Homes Group.

Plus, “smaller” deals, such as #1 D.R. Horton bringing SK Builders (#117 last year) into its fold and #36 Trumark Homes—also majority-owned by Daiwa House—expanding into the Pacific Northwest by acquiring Washington-based JK Monarch.

Since the beginning of 2024, 26 private home builder acquisitions have been recorded, according to Whelan Advisory Capital Markets, highlighting both increased competitive pressure and attractive exit opportunities for private builders.

“It is a sellers’ market for well-positioned private builders with significantly higher valuations,” says Margaret Whelan, the firm’s founder and CEO.

Why So Active?

There are several legacy and emerging reasons why M&A activity is on the rise lately.

Historically, builders looking to merge or (more commonly) acquire another builder are interested in entering or strengthening a market position, on the hunt for more land, or intrigued by new product type to meet market demand.

“It's easier to enter a market through acquisition than through a startup,” said former Toll Brothers CEO Doug Yearley at a housing symposium last June, also stating that he expected mergers among major public home builders to pick up and that the industry “deserves to be more consolidated.”

More recently, however, the field of buyers and sellers have become larger and more diverse than just the highest-volume, publicly held builders. Buyers now include private equity firms, Japanese conglomerates, and large private builders with access to publicly traded debt, not to mention the increasing influence of land banks to soften the blow to the buyer’s balance sheet.

“The increased universe of buyers is creating flexibility and creativity in deal structures, which allows for more transactions,” says Chris Jasinski, CEO & managing partner at JTW Advisors, a broker of several M&A deals in the housing sector. “Sellers have more options, and more types of options,” which has led to more lucrative deals.

Adds Whelan, “There are more buyers, with more money, from more places in the world trying to buy U.S. builders,” she says, driving up valuations for well-positioned private builders. “And different buyers are pursuing different strategies, which is why we’re seeing so much deal flow.”

The Impact on Housing

But beyond (or regardless) of that dynamic, and those who advocate for and profit from it, industry consolidation also has a dark side rooted in the savings and loan crisis in the 1980s and nurtured in the wake of the Great Recession that now appears to be undermining housing supply and affordability.

It also tracks back to a more recent fundamental shift among some at the top of the housing food chain that puts profits over product, hoards land with less debt, curries favorable financing, and vertically integrates to a greater extent—all of which arguably puts more money, power, and control in the hands of the few.

(And before you throw the “let the free market work” at me, think back to the liberally applied federal tax credits coming out of the Great Recession, namely the Worker, Homeownership, and Business Assistance Act of 2009, that financed the recapturing of key markets by large-volume builders for pennies on the dollar. It largely explains why the biggest builders emerged from the Great Recession with so little debt and the ability to acquire others.)

Profits Over Product

On a call reporting its Q3-2025 financial update, D.R. Horton, the largest home builder in the country by volume and home building revenue, told investors and analysts that it had “shifted its strategy from exponential growth … to returns-focused, disciplined capital allocation.”

Earlier that year, also with investors, PulteGroup’s CFO talked of “prioritizing price and margin over volume,” while Taylor Morrison’s 2025 Annual Report touted a strategic “reset” that includes “greater balance across starts, sales and closings and prioritizing returns over volume,” also arguing that fewer housing starts across the industry “will restore equilibrium over time.”

Translation: “We’re going to build fewer homes to achieve greater profitability and shareholder value.”

But it’s more than that. The strategy also earns investment recommendations from Wall Street and (through land banks that help reduce debt load) keeps buildable or developable lots out of the hands of smaller-volume, typically local builders or forces them to pay more for it, raising costs and further suppressing supply.

For some proof of that concept, consider these insights from Building the Bottlenecks: The Impact of Homebuilder Consolidation, a study released in December that tracked 73 M&As among the top 200 homebuilders between 2004 and 2019:

- Following a merger, new-home supply declined 7.6% in overlapping markets relative to non-overlapping markets;

- The merged builder reduces its output by 24.3% in overlapping markets after being acquired, and;

- The median price per square foot of new homes in that market rose by 6.7%.

If those numbers hold true for two recent deals, how might it impact attainability in the six markets shared by Taylor Morrison and Clayton Home Building Group (Berkshire’s stable of stick-builders), or the five overlapping markets between Stanley Martin Homes and United Homes Group?

Following a merger, new-home supply declined 7.6% in overlapping markets relative to non-overlapping markets, the merged builder reduced its output by 24.3% in overlapping markets after being acquired, and the median price per square foot of new homes in that market rose by 6.7%.

Land Banking Leverage

Not only does “disciplined production” among the publics and few large private builders mean fewer homes built, but their use of land banks to acquire most of the excess finished lots, land under development, and raw land in M&A deals allows acquiring builders to buy land-heavy sellers while incurring far less debt.

“Land banks have operated in the homebuilding industry for the past 25-plus years,” says Jasinski, but in the past five years, their presence has grown significantly in concert with the push for land-light business models. “It increases the number and types of deals that can be done.”

It also has enabled the top 10 home builders to currently own or control more than 1.86 million finished and unfinished lots, led by D.R Horton with 591,900 and Lennar with 506,000—roughly 59% of the total between the two.

That’s quite a script flip from a decade ago, when public builders owned about 64% of their lots and optioned the rest, a Business Insider stat reported in Capital Crunch: How the Fall of Local Finance and the Rise of Shareholder Primacy Warped Single-Family Homebuilding in America—And What to Do About It, a study released in November 2025 by the American Economic Liberties Project.

Today, those builders own or show debt against only 26% of their lots, almost the exact ratio of D.R. Horton’s current holdings, according to its 2025 annual report.

And since 2020, the ratio of lots controlled by public builders has increasingly exceeded their new-home completions, while the cost of land has increased about two and half times as much as that of cost of labor and materials in the past decade, further eroding affordability.

With that, the relative lack of debt that land banking affords also earns favorable investment recommendations by Wall Street analysts, which estimate an enviable average annual gross profit of 21.9% among publicly held builders.

The gambit also allows those builders to afford mortgage rate buydowns and other financial incentives to attract buyers and gives them more flexibility to adjust to market ebbs and flows, namely to access lots when there is profitable demand to produce homes or keep them in reserve until conditions improve, a distinct competitive advantage.

Over the past three decades, the center of the industry, the construction of the starter home that millions of people need, has been centralized in the hands of a small number of players.— Matt Stoller, August 2024

With that, the American Economic Liberties Project study found that land bankers “tend not to deal with small home builders very much, regardless of their creditworthiness, preferring to focus on large-scale deals with public home builders.”

No wonder 40% of this year’s Top 200 (and likely a higher share below them) cite “finding and entitling land” as their second biggest business challenge in our 2026 survey.

And even when smaller home builders have land, says the Capital Crunch report, “They often lack adequate financing options to develop the land themselves and sometimes end up selling it to the large homebuilders.”

All of that adds up to a Wall Street dynamic that generally loves the publics and seems happy to help finance their growth through acquisition and gain market share, while the vast majority of home builders face “[t]ight lending standards for construction and development loans,” according to a 2024 report by Fitch Ratings.

Vertical Integration

It’s not unusual to find a large-volume home builder offering a mortgage lending, title and closing services, and/or home insurance policies to their buyers. Such vertical integration ideally helps streamline the purchasing process while contributing to the bottom line. Good business if you can get it.

However, some watchdogs fear that the practice could extend further, to essentially dedicated land banking operations and acquiring brand-name building products and materials suppliers or launching their own brands as a source of revenue, internal cost savings well beyond national contracts, and further control of the markets in which they build.

The poster child of the former is Forestar Group Inc., a publicly traded residential lot development company that is 61% owned by D.R. Horton. The land bank holds lots in various stages of development in 64 U.S. markets, and sold 14,240 of them in its last fiscal year—83% of them to D.R. Horton’s home building divisions.

For the latter, look no further than Clayton Supply, the integrated products division of Clayton Properties Group that produces cabinets under the DuraCraft label and Lux-branded windows and doors exclusively for Clayton’s stick-built and HUD-code home builders.

Meanwhile, the Capital Crunch report found interest by private equity firms in acquiring and consolidating key trade partners such as roofing, HVAC, plumbing, and electrical to farm out to large-volume builders of which they may also have a stake.

Those skills command higher profit margins and offer steady revenue, are in demand from pros and consumers alike year-round and in any market condition, and are a lever to expand a geographic footprint.

The potential downshot of more vertical integration is, like land banking and favorable financing, one more “have” that squeezes the “have nots” in terms of costs, lead times, and housing production.

The potential downshot of more vertical integration is, like land banking and favorable financing, one more “have” that squeezes the “have nots” in terms of costs, lead times, and housing production.

An Era of Oversight?

Last October, land banking among the largest home builders caught the attention of President Trump, who posted on social media that those home builders were “sitting on two million empty lots, a record!”

Soon after, after the U.S. Department of Justice (DOJ) explored an antitrust investigation to assess whether the nation’s largest home builders were colluding to artificially affect housing supply and pricing.

More directly, business merger guidelines enacted by the Federal Trade Commission (FTC) and the DOJ in 2023 requires their review all M&As—including those involving home builders—that exceed $101 million.

In a May 2025 blog post by Jeff Brazel of John Burns Research & Consulting (JBREC), of particular interest to builders is the “30% rule” within those guidelines, which states that mergers resulting in a combined market share of 30% or higher on a market-by-market basis may be “impermissible.”

Based on JBREC’s analysis of the top 15 U.S. markets, two of them—San Antonio and Tampa—each have one builder with over 25% of new home sales, the former the result of Lennar’s acquisition of Rausch Coleman in 2025.

With that, the Capital Crunch study found that among the top 50 U.S. housing markets, #1 D.R. Horton, is the market leader in 16 of them, while #2 Lennar leads in 18. In multiple cities, they both have high market shares, and combined control nearly a third of the Houston-area market.

The big, final question, at least as this trend continues, is how small- and medium-volume builders will fare in the next bust cycle, and—like the leading financial institutions of the last major downturn nearly 20 years ago, will the largest home builders be considered too big to fail?

About the Author

Rich Binsacca, Head of Content

Rich Binsacca is Head of Content of Pro Builder and Custom Builder media brands. He has reported and written about all aspects of the housing industry since 1987 and most recently was editor-in-chief of Pro Builder Media. rbinsacca@endeavorb2b.com