Standards provide crucial communication, alignment and compatibility at an international, national, industry and individual organizational level. These standards, accessible to everyone from global powers to developing countries, from international corporations to the Mom and Pop small business, provide guidance and infrastructure, state of the art technical knowledge and management best practices. In a global environment they ease the crossing of borders, cultures and languages. They form the basis in building trust, avoiding conflicting standards, reducing technical barriers and therefore facilitate the achievement of regulatory compliance. By driving efficiencies and the diffusion of new products into the marketplace they increase export capacity, facilitate global trade, national competitiveness and economic growth. At an organizational level, they provide agreed metrics, the opportunity for benchmarking and improving existing effectiveness and efficiency. They impact organizations by reducing waste, defects, accidents, emissions, negative environmental impact, and liability while mitigating losses all aimed at reducing production costs. While doing this they also leverage the increase of supplier, employee, customer satisfaction and innovation through improved performance. All of which drives the penetration of foreign markets, the increase of sales and supports sustained growth and long term competitive advantage. The impact of standards is dramatic and on a global scale it allows organizations and countries to drive efficiencies and more effectively focus resources and priorities.

While standards have national and international impact as a whole, a key group of standards, ‘Management Leadership Standards’ have a significant impact. The international scale and range of issues that organizations have to deal with today create significant pressure on resources. Consider the BP Gulf oil spill or the Japanese tsunami and its impact on the international supply chain. The financial crisis, national food issues involving e-coli, international toy recalls due to hazardous levels of cadmium, IT security and Homeland Security. The global environment has not become slower or safer.

Key tools to dealing with this fast moving environment are the worlds most referred and implemented standards of Quality, Safety, Environmental, Social Responsibility and Risk Management. Combined they provide an infrastructure to manage the range of diverse variables such as those mentioned above while supporting strategic decision making and sustainability. At the core of this set of Management and Leadership Standards is ISO9001 (Quality Management System Requirements) critical to their integration and ISO31000 (Risk Management: Principles and Guidelines) which, while a new standard is one that has the potential to have the largest impact in the future.

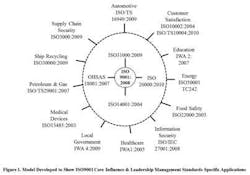

The tremendous impact of ISO9001 and ISO14001 on organizational practices and trade has stimulated the development of other ISO standards and deliverables that adapt the generic management system approach to specific sectors or aspects. The range of sectors and aspects can be seen in Figure 1 which highlights the broad influence and interaction of ISO9001.

Risks are a part of business, for many risk represents an opportunity for increased return and so for many it is considered fundamental to success rather being viewed as a negative. “The secret to systematic business model innovation is to focus on identifying where the risks are in your value chain. Then determine whether you can reduce them, shift them to other people, or even assume them yourself. If you take this approach, you won’t need extensive experimentation and prototyping to identify very powerful innovations because many tools for managing risk are available.” (Girotra & Netessine, 2011, p103) Indeed by using Standard and Poor’s newly available risk management rating, McShane et al found evidence of a positive relationship between increasing levels of risk management capability and firm value. (McShane et al, 2011)

But risk management ‘capability’ is the key. Most companies do not have a structured risk management system in place but rather have informal approaches. (Christopher et al, 2011) With65% of businesses not conducting systematic risk analysis prior to major corporate decisions and only 42% conducting risk management audits or procedure compliance (FERMA, 2010) risk for the majority is not well enough managed to be an opportunity.

For an earlier blog overviewing risk sources and steps for risk management see:

http://www.housingzone.com/blog/risk-management

REFERENCE:Denis Leonard, The Efficiency Impact of International Standards on Global Trade, National Industries and Individual Organizations: The Influence of Quality and Risk Management, Standards Engineering: The Journal of the Standards Engineering Society, January/February, Vol 65, No 1, pp 1-8, 2013.

http://businessexcellenceconsulting.net/files/impact_of_int_stds_quality_risk_mgt_denis_leonard.pdf

About the Author

Denis Leonard

Denis Leonard has a degree in construction engineering, and an M.B.A. and a Ph.D. in quality management. He is a Fellow of the American Society for Quality and has been an Examiner for the Baldrige National Quality Award Board of Examiners, a Judge on the International Team Excellence Competition, and a Lead Judge on the National Housing Quality Award. He has experience as a quality manager in the home building industry as well as construction engineer, site manager, and in training, auditing, and consulting with expertise in strategic and operational quality improvement initiatives. His work has achieved national quality, environmental, and safety management awards for clients.